Solar PV in Italy

During the last 5 years, Italy has set new and ambitious targets in terms of carbon emissions, renewable energy deployments and carbon neutrality. Major target, which is to reach 100% Carbon Neutrality, is set to be achieved by 2050.

During the last 5 years, Italy has set new and ambitious targets in terms of carbon emissions, renewable energy deployments and carbon neutrality. Major target, which is to reach 100% Carbon Neutrality, is set to be achieved by 2050.

Renewable Energy is assumed to be the main driver and the main focus of the country to reach carbon targets, thus total share of Renewables is set to reach 30% in Total Energy Consumption and 55% in Electricity Production by 2030.

Although Renewables might be seen as they are at the centre of the focus, we see several impediments and, apparently, Italy has pinned its hopes on some other resources which may fail in the long run, such as Hydrogen and Carbon Capture. Around 500 mn Euro budget was spared for Hydrogen Research and Development.

Renewable Energy development faces several local and central resistance due to existing laws and regulations. Just after the launch of the Russian invasion towards Ukraine, Italian Government introduced new mechanisms to ease up Renewable Energy Project Development procedures and overcome long and thorny administrative impediments that makes permitting procedures extremely difficult. However, old habits resist against the new schemes and we hope the local institutions, and central ones to some extent, will comply in a better manner than it is today.

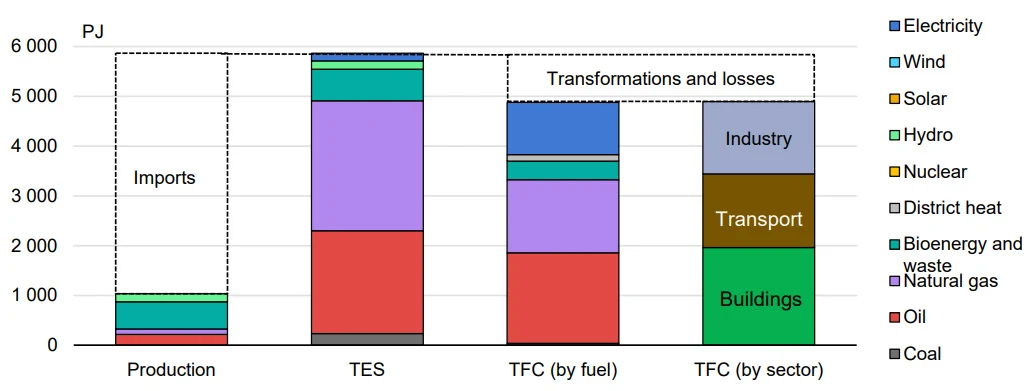

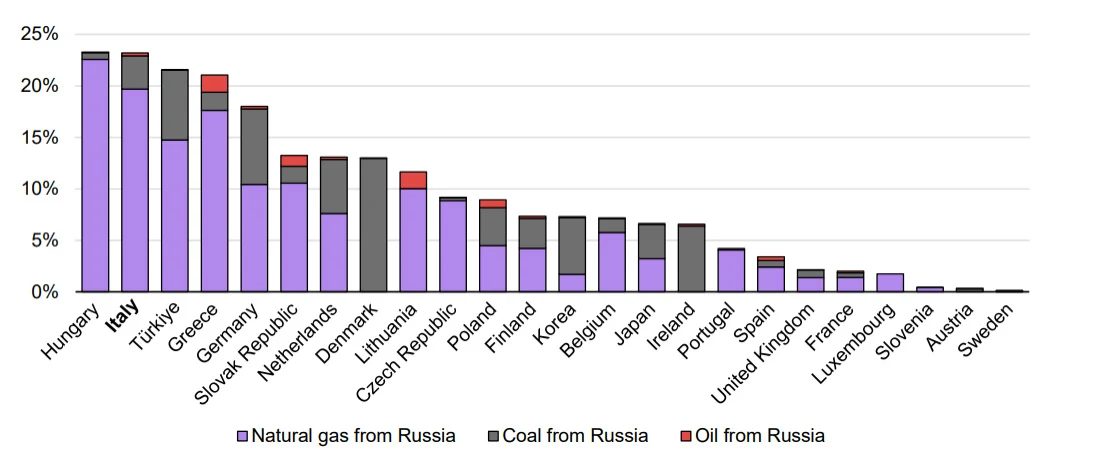

Italy imports more than 75% of its primary energy, Natural gas and oil, of which 41% is imported from Russia in 2021 together, dominate the energy pool. Coal is not substantial. Buildings are the major end users together with Industry and Transport.

Italy in 2022 started reducing Russian natural gas imports, by signing new contracts with alternative suppliers as well as reducing overall demand for natural gas through Renewable Energy Developments and energy efficiency, especially in the building sector.

| Indicator | Italy, 2021 |

|---|---|

| Electricity generation | 287.0 TWh (natural gas 50.2%, hydro 15.8%, solar 8.8%, bioenergy and waste 7.5%, wind 7.3%, coal 5.6%, oil 2.7%, geothermal 2.1%), -5% since 2011 |

| Electricity net imports | 42.8 TWh (imports 46.6 TWh, exports 3.8 TWh) |

| Electricity consumption | 300.6 TWh (industry 46.9%, service sector buildings 27.0%, residential buildings 22.4%, transport 3.7%), -4% since 2011 |

| Peak load | 55.2 GW (July 2020) |

| Installed capacity | 118.4 GW (2022) |

Although it looks Italy is on track to reach its National Energy and Climate Plan (NECP) for 2030, further aggressive measures need to be taken to reach 2050 targets and in particular, possible new requirements to be imposed by EU, due to FiT-for-55 (FF55) package.

From time to time, it appears so, we have the feeling that Italy’s main focus is, instead of reaching 100% Carbon Neutrality through Renewables, to cut-off Russian imports and to find alternative Gas and Oil routes and to use Natural Gas for Hydrogen production.

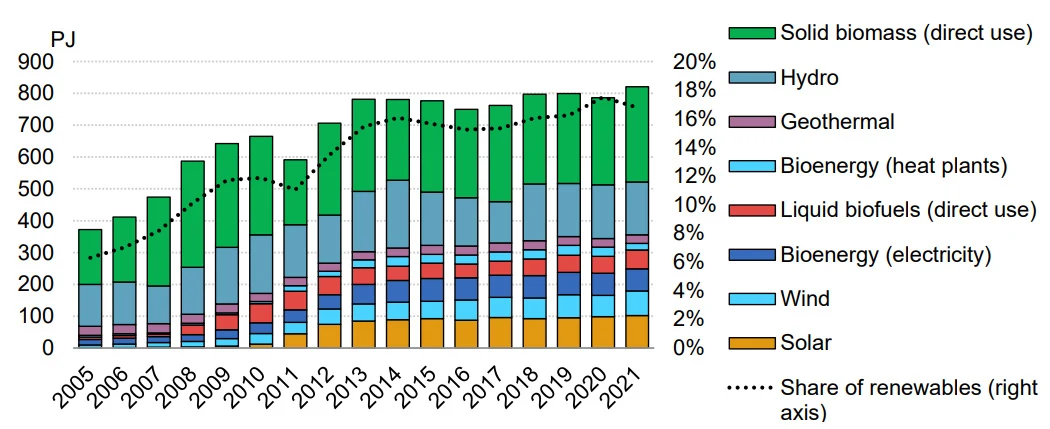

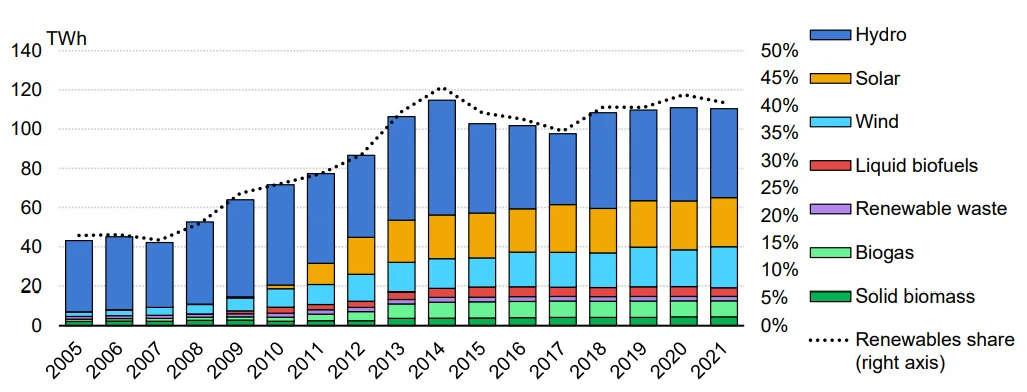

According to the IEA report, the share of renewables in total final energy consumption has increased from 7% in 2005 to 16% in 2014 and in 2020, the share of renewables increased to 18%, mainly as a result of new Solar and Wind Power Plants.

Bioenergy is the main renewable energy source, Hydropower comes as the second largest renewable source of energy, which accounted for 55% and 20% of renewables use in 2021 respectively.

To achieve the 2030 targets, the NECP (National Energy and Climate Plan) mainly points towards the expansion of wind and solar electricity generation particularly agri-PV.

| Renewable energy share | 2021 status | 2020 targets | 2030 targets NECP | 2030 FF55 targets (provisional) |

|---|---|---|---|---|

| Overall target (renewables in gross final energy consumption) | 19.03% | 17% | 30% | 36.7% |

| Electricity | 36.0% | 26.4% | 55.4% | 65% (a) |

| Heating and cooling | 19.71% | 17.1% | 33.9% | 40% |

| Transport | 10.0% | 10.1% | 21.6% | -13% (b) / 28% (c) |

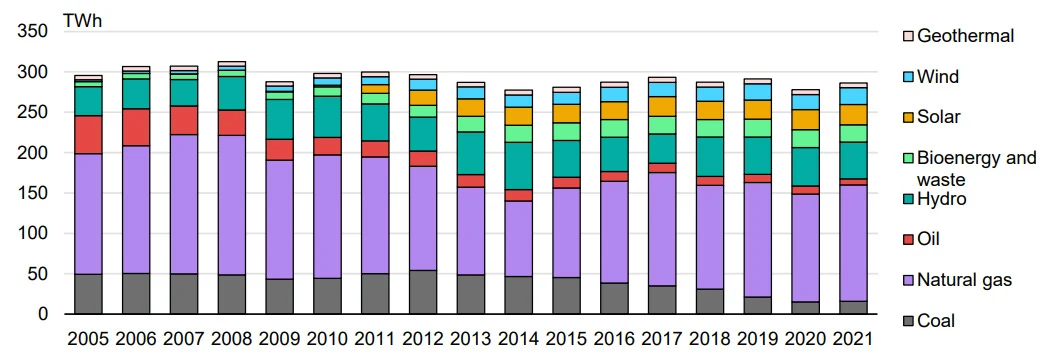

Renewable sources’ share in electricity production increased by more than 100% between 2005 and 2021. It accounted for 40.5% of total electricity generation in 2021 and 36% of gross electricity consumption in 2020. Overall, between 2010 and 2020, generation from Solar PV increased by more than twelve-fold. This increase was mainly due to the incentives that were provided before 2016. This upwards trend is continuing and the share of Solar PV shall increase dramatically in the coming years thanks to the major drops in solar LCOE (Levelised Cost of Electricity) bringing solar below the Grid Parity. After a steady period of Solar PV from 2017 to 2020 we shall see more and more Solar PV domination.

According to the NECP, by 2030, installed solar PV capacity should increase from 24.2 GW in 2022 to 52.2 GW, which points to a 31 GW additional capacity. Where, wind capacity should increase to 19.7 GW from its 11.7 GW 2022 level. Please note that Solar PV has already reached 29 GW by the end of 2023.

| Renewable electricity capacity (GW) | 2022 status | 2030 NECP targets | 2030 FF55 target (provisional) |

|---|---|---|---|

| Variable sources | 35.9 | 71 | 87 |

| PV | 24.2 | 52 | 64 |

| Wind | 11.7 | 19 | 23 |

| Non-variable sources | 27.4 | 24 | 27 |

| Hydro | 22.8 | 19 | |

| Other (including biomass and geothermal) | 4.6 | 5 | |

| TOTAL | 63.3 | 95 | 114 |

Solar Project Development in Italy

Around 3.8 GW of Solar PV was deployed in 2023, bringing the total Solar PV capacity to around 29 GW in Italy. The country is very attractive for Solar Project development for various reasons.

High irradiation rates, lower LCOE, big population, energy consumption, Grid Infrastructure although additional investments are required, highly developed private sector and industries, thus private consumers, availability of the PPAs with private consumers not only in Italy but also in other parts of Europe, integrity to the EU inter connection and financial system, well developed free electricity market, increasing electricity demand in summer time which corresponds with the peak solar PV production, penetration of electric vehicles, limited local gas and oil resources and ambitious Solar PV targets are the basic reasons which make Solar PV more attractive.

Italy is from time to time busy with Hydrogen and Carbon Capture developments. We see that these developments are consuming the valuable time and resources. Hence, the National Recovery and Resilience Plan (NRRP) stated that developing hydrogen as indicated by the preliminary guidelines would require about EUR 10 billion in investments until 2030.

Although some see that Natural Gas could be used for Hydrogen production, cheap Solar PV is planned to use for that. It is always more environment friendly and economic to use the electricity from Solar PV. In any case, it is not hard to see that Solar PV shall dominate Italy’s future energy production.

The competition is tough, almost all of the world energy giants are already in Italy and developing & building Solar PV projects. Therefore, it is not easy to take place in the market, however we still see a broad room for opportunities in Italy.

There are of course several key factors for success.

Investors should:

- Learn the Project Development Sub-Regulations, namely; AU, PAS, DILA, Comm. to the Municipality and Free Building Development

- Understand pros and cons of each

- Understand which sub-regulation fits its needs

- Decide the size of the prospect PV projects based on needs

- Choose a trustable developer

- Understand the land types and secondary land regulation

- Select the appropriate land type

- Find the land, implement a land DD, check the constraints

- Select the appropriate capacity for each prospect project

- Check the availability of the Grid

- Understand the permitting processes and the approval authorities

- Understand the costs and build a reasonable and correct budget

- Foresee the expected time lapses

- Find appropriate project design companies

- Understand the agri-PV regulations, if needed

- Try to understand the nature of PPAs and see if they are suitable

- Try to understand not only the local but European wide finance opportunities

- Try to understand the wholesale electricity prices and the market.

2026 Update

This section was added by the solarVis editorial team on 30 July 2026. Everything above is Cem Göçmen's original analysis, published on 15 February 2024 and left unchanged. Several of the frameworks it describes have since been replaced, so the update below records what changed rather than editing the original.

The 2030 targets were raised

Italy submitted an updated National Energy and Climate Plan (PNIEC) to the European Commission on 1 July 2024, and it supersedes every 2030 figure in the analysis above.[2] The renewable share of gross final energy consumption moves from 30% to 39.4%, the renewable share of electricity from 55% to 63.4%, and the solar PV capacity target from 52 GW to 79.2 GW. Wind rises from 19 GW to 28.1 GW, within a total renewable capacity target of 131 GW. The ETS-sector emissions target is a 66% cut against 2005, ahead of the 62% the EU requires.

| 2030 target | 2019 NECP | Updated PNIEC (July 2024) |

|---|---|---|

| Renewables in gross final energy consumption | 30% | 39.4% |

| Renewables in electricity | 55% | 63.4% |

| Solar PV capacity | 52 GW | 79.2 GW |

| Wind capacity | 19 GW | 28.1 GW |

| Total renewable capacity | not specified | 131 GW |

Capacity grew fast, then slowed

Italian solar PV passed the 29 GW quoted above and kept climbing: 37.0 GW at the end of 2024, 43.5 GW at the end of 2025, and 46.6 GW across 2,255,654 plants at 30 June 2026.[3][5] Annual additions tell a less comfortable story. After 6.8 GW in 2024, Italy connected 6.4 GW in 2025, its first annual decline since 2013.[4]

Sources: GSE, Terna, ITALIA SOLARE, MASE

The 2025 figure is the first annual decline since 2013. The 2026 bar covers the first half of the year only.

Sources: Terna, ITALIA SOLARE

The slowdown is concentrated in the small-scale segments. Residential installations fell 32% in 2025 and commercial and industrial capacity dropped 26%, while utility-scale connections grew 15%. For developers, that is the most consequential line in the whole update: the Italian market is rotating from rooftop volume towards large ground-mounted projects.

Residential is derived as the balance of the 6,437 MW national total after the reported commercial, industrial and utility-scale figures.

Sources: ITALIA SOLARE

At 46.6 GW in mid-2026, reaching 79.2 GW by 2030 means adding roughly 7.2 GW every year. Italy delivered 6.4 GW in its best recent year and is running below that pace in 2026.

Permitting was consolidated into three tiers

The sub-regulations in the checklist above, AU, PAS, DILA, notification to the municipality and free-building development, no longer describe the Italian system. The Testo Unico FER, Legislative Decree 190/2024, came into force on 30 December 2024 and replaced that patchwork with three regimes: attività libera, requiring no consent or declaration except where landscape constraints apply; PAS, a simplified enabling procedure; and Autorizzazione Unica for larger projects.[6] The single application models followed in December 2025 and by ministerial decree 223 of 15 July 2026.

Agricultural land closed, agrivoltaics opened

Decree Law 63/2024, converted by Law 101/2024 in July 2024, prohibits new ground-mounted PV in agricultural zones, leaving only narrow exceptions for quarries under environmental restoration and closed or restored landfills.[7] Agrivoltaics, where elevated modules let cultivation continue, is explicitly exempt, and that exemption has redirected much of the Italian ground-mount pipeline towards agrivoltaic, brownfield and industrial-adjacent sites.

The suitable-areas framework also changed twice. Article 7 of the June 2024 decree was annulled by TAR Lazio in judgment 9155 of 13 May 2025, partly because regions had drawn buffer zones of up to 7 km around protected assets.[8] The regime then moved into primary law: Law 4 of 15 January 2026 inserted article 11-bis into the Testo Unico FER, expanding the areas that qualify by statute, capping regionally designated suitable agricultural land at between 0.8% and 3% of each region's utilised agricultural area, and defining agrivoltaics for the first time, with a certified requirement to preserve at least 80% of gross saleable agricultural production.[9] Authorisation procedures already pending on 22 November 2025 stay under the previous rules.

FER 1 gave way to FER-X

The incentive landscape has been rebuilt. The FER-X Transitorio scheme replaced the expired FER 1, and its first auction, published on 1 December 2025, awarded 7,697.6 MW to 474 solar plants at a capacity-weighted average of 56.825 EUR/MWh, an average discount of 37.34%, against 17,537 MW of expressions of interest.[10] The definitive scheme was signed on 18 June 2026 with a 37.15 GW contingent, 10 GW of it for solar, awarded through 20-year two-way contracts for difference.[11] Italy also completed its RED III transposition with Legislative Decree 5/2026, in force on 4 February 2026.[12]

Prices are high, and the grid is the binding constraint

Italy had the most expensive electricity in the European Union in 2025, averaging 116 EUR/MWh on the day-ahead market against an EU average of 85 EUR/MWh.[13] Worth noting for anyone modelling revenue: the Italian market applies a zero floor rather than allowing negative prices, and on 1 May 2026 the PUN Index sat at exactly zero for six consecutive hours nationwide for the first time.[16] Curtailment risk, not negative pricing, is the Italian version of this problem.

The PPA market the article recommends studying has matured. Italy was the second most active in Europe in 2025 with 1.6 GW across 26 deals and solar PPA volume up 184%.[17] Indicative early-2026 ranges are roughly 48 to 65 EUR/MWh for utility-scale plants and 58 to 78 EUR/MWh for commercial ones, though index quotes sit above transaction averages.[18]

Grid access is now the real bottleneck. Renewable connection requests to Terna stood at 341 GW in September 2025, more than four times the entire 2030 solar target, against 46.6 GW actually built.[19] Italy's electricity interconnection level is 5.13%, well short of the EU's 15% goal for 2030, and Terna's 2025-2034 development plan commits more than 23 billion EUR over ten years to address it.[20][13]

Gas, coal and hydrogen

The import picture the article describes has largely resolved. Russian gas fell from 41% of Italian gas imports in 2021 to less than 3% of gas demand in 2025, some 1.5 bcm delivered entirely as LNG, with Algeria now the largest supplier.[13][1] Solar generated a record 44 TWh in 2025, up 25.1%, covering 14.5% of demand, while renewables overall covered 41% of demand against 42% in 2024 as hydro normalised after an exceptional year.[14]

Coal moved the other way. Italy had planned to leave coal in 2025, but an amendment approved on 27 March 2026 pushed the phase-out to 2038 after the gas price shock of early 2026, keeping the Brindisi and Civitavecchia plants on standby.[15]

On hydrogen, the caution in the original analysis reads well. Italy published a National Hydrogen Strategy in November 2024 whose domestic-production scenario requires 15 to 30 GW of electrolysers and 8 to 16 billion EUR of investment by 2050, against more than 6 billion EUR of public resources currently available.[21] The competition between hydrogen and cheap solar electricity for capital and attention has not been settled.

Frequently asked questions

References

- IEA, Italy 2023 Energy Policy Review

- MASE, Italy's updated National Energy and Climate Plan (PNIEC), submitted 1 July 2024

- GSE, Solare Fotovoltaico, Rapporto Statistico 2024

- ITALIA SOLARE, first decline in installed solar capacity since 2020 (7 February 2026)

- ITALIA SOLARE via SolareB2B, 3.1 GW connected in H1 2026

- Legislative Decree 190/2024, Testo Unico FER, in force 30 December 2024

- Decree Law 63/2024 converted by Law 101/2024, restrictions on ground-mounted PV on agricultural land

- TAR Lazio, judgment 9155 of 13 May 2025 annulling article 7 of the suitable-areas decree

- Law 4 of 15 January 2026, suitable areas and agrivoltaics moved into article 11-bis of Legislative Decree 190/2024

- GSE, FER-X Transitorio first auction results, 1 December 2025

- MASE, FER-X Definitivo signed 18 June 2026, 37.15 GW contingent

- Legislative Decree 5/2026, Italian transposition of RED III, in force 4 February 2026

- European Commission, REPowerEU Four Years On, Italy country assessment (22 April 2026)

- Terna, Italian electricity consumption in 2025

- Enerdata, Italy delays its coal power phase-out to 2038

- GME data via Rinnovabili.it, PUN Index at zero for six consecutive hours on 1 May 2026

- Pexapark data via Strategic Energy Europe, European PPA market 2025

- Solar Data Atlas, indicative European solar PPA price ranges (March 2026)

- Terna Econnextion data via QualEnergia, renewable grid connection requests

- Terna, Development Plan 2025-2034

- MASE, National Hydrogen Strategy (November 2024)